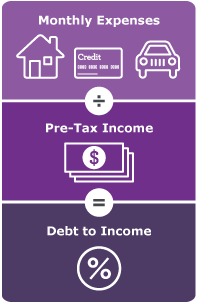

From a credit perspective any things can be weighed in to determine how a lender can look at to determine eligibility for a loan. One such variable is what is called the debt-to-income ratio. This ratio is something that can determine your inflow vs outflow of money that you use for paying any debtor.

The debt-to-income ratio (commonly referred to as DTI ratio for short) is the percentage of your gross monthly income that goes to paying your monthly debt payments and is used by lenders to determine your borrowing risk. A low DTI ratio demonstrates a good balance between debt and income, while a higher ratio determines there is more going on behind the scenes. The maximum DTI ratio varies from lender to lender. However, the lower the debt-to-income ratio, the better the chances that the borrower will be approved, or at least considered, for the credit application. An ideal formula for determining DTI would be to divide the number of the total monthly debt payments (credit cards, loans, mortgages, rent etc.) over the total of gross monthly income (your income before tax and deductions). For example, if john owes $1200 in his monthly bills and his gross income is $2700 per month his overall DTI would be $1200/2700=0.44 or 44%. John has a more moderate debt to income ratio based on these figures.

One can lower their debt-to-income ratio by reducing their monthly recurring debt or increasing their gross monthly income. Using the above example, if John has the same recurring monthly debt of $2,000 but his gross monthly income increases to $8,000, his DTI ratio calculation will change to $2,000/$8,000 for a debt-to-income ratio of 0.25 or 25%. Similarly, if John’s income stays the same at $6,000, but he can pay off his car loan, his monthly recurring debt payments would fall to $1,500 since the car payment was $500 per month. John’s DTI ratio would be calculated as $1,500/$6,000 = 0.25 or 25%. If John can both reduce his monthly debt payments to $1,500 and increase his gross monthly income to $8,000, his DTI ratio would be calculated as $1,500/$8,000, which equals 0.1875 or 18.75%. Ideally renegotiating interest rates, aggressive payment schedules including principal payments and generating more income through a second job or a side gig for other active or passive income are some ways that people have taken to rapidly clear up debt and improve their ratios

The DTI calculation in assessing the risk that a borrower poses to a lender in terms of their ability to repay. The lower their ratio (such as 35% or less as noted by an average between different lending companies and financial institutions) can be considered more favorable. Meanwhile a DTI of 36-49% leaves room for improvement and can be steered into a more manageable direction with proper education and action plans. For a DTI above 50% it is generally considered difficult for a borrower or spend or save as their money for unforeseen circumstances. The higher the DTI the more likely a borrower could be inversely impacted by any major financial event and presents more of a risk of default to a lender. The ideal situation for a customer and a lender is to be at a point where any new debt ought not to put the borrower or the organization doing the lending in an adverse situation that would harm the institution with a loss or damage an individual’s credit.

The Debt-to-income ratio is a commonly questioned concept for credit building and lending by consumers. I hope my summary of what DTI is and how it affects you will give you more insight to how to further gain more perspective on your own credit journey. For your convenience I have also included a link for a DTI calculator for you to plug and play with figures to see how your own DTI is faring. Until the next time dear readers. Excelsior!

/what-happens-if-you-dont-pay-a-collection-960591-v3-5bbe02b546e0fb00510fde7e.png)

/GettyImages-140671550-56a636e83df78cf7728bdbc1.jpg)