Going into the new year, I have quite a few goals to accomplish. This is normally the time when we would all set a New years resolution. We can set goals, but when we lack directon and consistency, we end up short. This issue is best tackled by SMART goals.

A SMART goal is one that is specific, measurable, achievable, realistic, and timley. Defining these parameters as they pertain to your goal helps ensure that your objectives are attainable within a certain time frame. An example of this would be: losing 20 pounds by the end of the year. To track progress, someone might do morning or weekly weigh-ins to gauge progression. Additionally, changes to ones diet and exercise regimine will aid in the process. As time goes on, one will be able to see how progress is going along to see if progress is being made in a timely fashion. If things are not being done in time, there are metrics that might need to be updated, like eating even more differently and lifting more weight and longer, more intense cardio sessions. These metrics will change as time and circumstances change.

No matter what your goal is, in order to obtain it, there must be purpose and direction as we as a way to monitor progress. A SMART goal is a specific way to measure out and make your goals more attainable in a realistic and timely fashion. Going into the new year, i encourage you to make SMART goals to have a successful new year. Until the next time, dear readers, excelsior and happy new year!

As a finance professionL I am asked a myriad of different questions in regards to personal finance. From simple questions on account balances to the fine workings of credit, there is never a dull moment or a dull question. One common misconception I have seen is what a line of credit is and exactly how it works.

A line of credit is a revolving line of credit (similiar to a credit card) that allows you to access money as you need it up to a certain limit. You can borrow up to that limit again as the money is repaid over time. A line of credit requires approval by a bank or credit union through various criteria such as credit, income, and other factors that a lender may require. Once funds from a line of credit are used, interest will accrue until the loan is repaid.

Unlike traditional personal loans (and most credit cards), the interest rate on a line of credit is generally variable, meaning it could change as broader interest rates change. This can make it difficult to predict what the money you borrow will end up costing you over time.

Generally speaking, lines of credit aren’t as common as their counterparts know as home equity lines of credit or HELOCS (we’ll visit this later). These see usage for various things such as home improvement projects, weddings, unexpected repairs, and other things that might not have a certain upfront cost. Additionally, there may be other costs associated with the line of credit, such as maintenance fees. Be sure to consult your lender in regards to learning all fees associated with a line of credit. Credit cards will always have minimum monthly payments, and companies will significantly increase the interest rate if those payments are not met. Lines of credit may or may not have similar immediate monthly repayment requirements.

In summary, lines of credit are useful tools that can benefit you if there are things that are appropriate to use it for. They aren’t common, but whether it be for a person or for a business, a line of credit can be a viable asset to move things along. Until the next time dear readers. Excelsior!

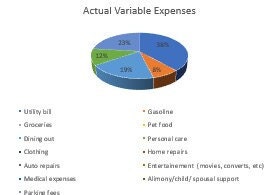

I wanted to take a moment to share my latest project I’ve been working on that is very near to my heart. I have been working on a monthly budgeting tool with a few extra goodies to help highlight where money goes and helps track where one is compared to their projections. This is a great tool that can be reused easily and can even help you recognize where you are in terms of building your net worth. Click here to view my monthly budgeting tool.

A snippet of a chart from my planner detailing spending categories

I still have my latest entry aside from my update in store for later this month. Stay tuned dear readers for the next entry! Excelsior!

Building credit takes time. As I often tell my clients: credit building is a marathon rather than a sprint. The age of credit is an often misunderstood concept as in today’s fast paced society it is something that can be very important to improve credit history.

The average age of accounts is one of the factors that contribute to your overall Length of Credit History, which itself accounts for 15% of your total FICO credit score. This is calculated as a simple, non-weighted average; it’s the sum of the ages of your credit accounts divided by the number of accounts that you hold. These are also ranked in importance: the age of your oldest account, average age of accounts, and age of your newest account.

When you close a credit card, it can stay on your credit report and continue to age for 10 years. This means that you could open a credit card today, cancel it tomorrow, and 9 years from now, it would still show up on your credit report and contribute to your credit history.

An example of this would the average of your credit cards. Card 1 is 7 years old, card 2 is 3 years old and card 3 is 2 years old. We could take the average between the 3 cards to obtain an average age of 4 years between all credit cards. If you close one of the cards and fast forward 10 years card number 1 is now 17 years old, card 2 is 13 years old and card 3 is 12 years old. Taking your average age of accounts to 14 years old. This can still be in effect due to credit card accounts lingering on your credit report can still effect your history for up to 10 years. The most important concept to remember is not to close the longest (oldest) open trade as this will hurt your average age of your accounts and your credit score. Closing the newer cards will have less of an impact due to them being newer, but it is important to remember when closing a credit card that there is credit capacity (amount of available credit vs amount of credit used) that is lost when this happens. If the capacity is reduced thus will also hurt your score if your balances are too high on your remaining cards. Only close out credit accounts as needed (if they’re not installment loans of course).

Credit utilization can be tricky but if one knows how to navigate the complexities it can be a rewarding tool. Letting time work it’s magic on your open credit accounts cab do wonders for your score. Until the next time dear readers excelsior.

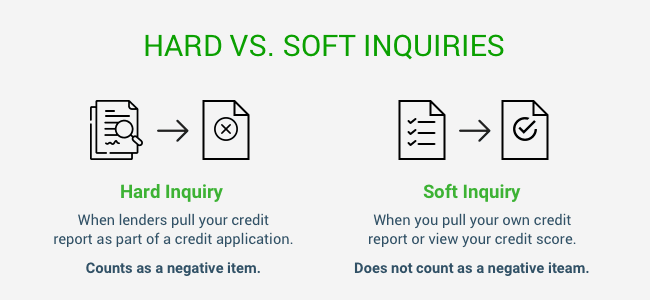

In the world of credit there are many different factors that build and tear down a score. One common conversation I often have in regards to credit is regarding inquiries. There are many misconceptions as to what an inquiry is and I will explain and debunk these misconceptions in this post.

Inquiries are entries that appear on your credit report when your credit information is accessed by a legally authorized person or organization (including yourself). Most commonly, inquiries are the result of an application for credit, goods or services, an account review made by a company that you already do business with, or a preapproved offer of credit that has been sent to you.

There are two types of credit inquiries: hard inquiries and soft inquiries. Account reviews and preapproved offers fall under the category of soft inquiries, which have no effect on your credit scores. Hard inquiries include applications for credit or certain services, and although their impact is minimal, they can temporarily affect your scores. It is good practice to get your credit report checked throughout the year to view hard and soft inquiries.

A hard inquiry appears on your credit report when a lender checks your credit in response to an application for a new loan, credit card or line of credit. Whenever you seek new credit, there’s the potential for a new debt, which may temporarily lower scores slightly until you can show that you are managing that new debt responsibly. Credit scoring models such as those from FICO or Vantage sometimes account for that increase in risk by lowering your scores slightly. Typically, most score models show hard inquiries typically lowering scores by less than five points.

Hard inquiries remain on your credit report for up to two years, but as long as you keep up with your payments, credit scores often rebound from an inquiry within a few months. And, most credit scoring models no longer count a hard inquiry in score calculations at all after 12 months.

Soft inquiries appear on your credit report when someone runs a credit check for reasons unrelated to lending you money. These events are not associated with greater repayment risk, so they have no effect on your credit scores. Common examples include but are not limited to: utility companies for services and equipment, auto insurance companies, credit card companies that you have accounts with currently, as well as a credit review with a lender in a bank or credit union.

It is ideal not to accumulate too many inquiries as they can lower your scores over time if one is rapidly shopping for credit. There are an exception to this however. If there are multiple inquires from a car dealership to other lenders when you finance a car (this is called shotgunning the credit as it goes to mulltiple lenders) within a certain period of time it is counted as one inquiry. Inversely, if there are multiple inquires foe different types of credit in a period of time that is a sign of concern to a lender. It is important to check your score reports at least once a year to ensure all inquires on your report were authorized as unfamiliar inquiry activity could be a sign of either an error or criminal activity. You can review your annual credit report for free Here.

Inquiries are as I call the “cost of admission to credit”. These inquires make up a small percentage of your credit score but it is important to not go overboard with shipping for credit and recognize that even if they are small, inquires can still have an effect on your credit score. Until the next time dear readers, excelsior.

In my realm of expertise, I have been exposed to credit ranges across the spectrum. Some are great, some are good, some are ok and some need work and that’s alright with me. Credit is something that some treat like a sprint, but it truly is more of a marathon. Some treat some items on their credit (collections, current payment history, credit card limits, etc.) as an individual guitar solo rather than looking at all the items on their credit report as a symphony. One common thing I come across is a combination of income and credit. You could make excellent money, but your credit could be excellent, fair, poor, or nonexistent. I have also seen the inverse with those that make less money as well in addition to those in the middle of the income ranges, I have seen. A concept that eludes some of us is the concept of having limited credit.

The terms “limited credit” and “no credit” are typically used synonymously to describe anyone who has not been the primary account holder on a credit card or loan for three years. This is something commonly seen with those that have bought everything with cash only or just never had a need to get anything on credit. Additionally, some lenders might not even report to the credit bureau which is what sometimes is referred to as “invisible credit”. If you suspect your credit history is insufficient because of a data problem, contact your lenders and check whether your personal information on file with them is correct (i.e. name, date of birth, social security number, etc.).

Lending companies/financial institutions give inexperienced consumers the benefit of the doubt to a certain extent in that the terms they offer them are better than those given to people with bad credit. However, you must demonstrate the ability to consistently make on-time payments to your monthly financial obligations as well as maintain balances below your credit limits in order to build the requisite credit history to be trusted with higher credit lines as well as competitive rates and rewards. An example of this would be if someone with limited credit requests a loan for a new auto. With zero history (keeping in mind your credit report is like your report card for your credit) it isn’t normal to see high balance loans for an auto with such limited history (unless there is a very good strong cosigner or a significant down payment). Without a down payment or cosigner, there’s a good chance that you could end up with a smaller car loan to start out (even if you make excellent money) due to the lack of history to prove creditworthiness based on the risk to the lender or receive a denial for credit. Once the loan has been successfully paid off (and provided a great pay history) that loan could be used as the basis for another perhaps larger loan in the future.

No matter what age you are or where you are in your credit-building journey, a lender typically relies on a credit score to help decide whether to approve you for a credit card or loan. There are numerous ways today to build your credit. From online banks to even your own bank or credit union there are programs designed to start off your credit journey before your next big purchase. From share-secured loans to secured credit cards, there are ample opportunities to build credit in today’s times. Consult your local bank/credit union for different credit building products to help you in your financial journey. Until the next time dear readers. Excelsior!

I am a firm believer in moving in silence. I keep my best work close to the chest. I have been working on a small project of mine for a little while and I have been waiting for the right time to share what I have been up to: I am officially a published author!

This is a short read but I am a believer in quality over quantity. I wanted to highlight some of my own life experiences during my initial foray into the corporate world. I elected to highlight my post college search for my first full time position and the lessons I have learned during that time. Originally, this was wrote in a journal format as I went along with my search. I had to make some modifications to the formatting to make it less like a journal and more like a guide with lessons Iearned during this point of my life.

I was quite nervous when the time came to publish but when I got the initial proofs I couldn’t help but to smile like a proud parent. This is the first work I’ve completed and I have more to come in the future. I have attached a link to find my work on Amazon here for those who would wish to see my latest work.. In the meantime, stay tuned for my next posting. Until the next time my friends, excelsior!

A message on a credit report that can pop up is “insufficient credit”. This is a message commonly found for those who are young, operated primarily with buying things cash, or perhaps haven’t taken out a form of credit in a very long time. This isn’t necessarily a good or bad thing, but rather a good launching point towards developing health credit.

When applying for credit, lenders are only allowed to use a specific set of criteria to evaluate an application. Insufficient credit history indicates that the applicant doesn’t have enough accounts with a long enough payment history to approve an application. Banks, cell phone companies, and utility companies also look at this information when you set up a new account. As an applicant applies for bigger loans, lenders want to see that an applicant can handle multiple accounts responsibly. If someone only has a single credit card or too few accounts overall this could be a reason for rejection on a credit application.

On the other side of the coin, one wouldn’t want to go opening too many new accounts in a short time to build credit. On average it takes a minimum of 6 months for a new trade to make progress on an individual’s credit rating. Opening too many would be classified as an escalation of new debt. This could also be a reason to deny an applicant on a credit application. On another note, if there isn’t an update in activity (such as a credit limit increase or a new line of credit) for a substantial period, an individual’s credit could become stale and outdated causing it to be insufficient again. Keep in mind that the age of active credit lines also helps in building a score over time. These trades could be a line of credit or a credit card primarily.

Updating the personal information in one’s credit history is relatively easy. Building up one’s credit history takes more time and credit experts emphasize that there is no quick fix to a credit score. Experts typically recommend a few ways to help keep things in a positive light for one’s credit: 1) pay all bills on time to avoid them going into a collection action 2) opening a secured credit card or secure loan of some sort to start a history 3) reporting non-debt obligations If your lender uses a scoring system that counts that among other ways. Some lenders will overlook an insufficient credit history if the applicant is strong in other areas such as in debt-to-income ratios and stable proof of income to show how one could make payments.

Keep in mind that another common misconception is that checking accounts, debit cards and credit union accounts do not build credit. The checking account is designated for expenses and the debit card can be run as “credit” but is not truly linked to a credit line. Credit union accounts give you access to the credit union and all its services such as lending and credit building programs.

Having insufficient credit can be difficult and confusing at times, but it doesn’t have to be. Feel free to reach out to your local financial experts at your financial institution and ask for ways to help establish a credit history for yourself. It will take time but the result of a healthy score and better rates are worth it. Until the next time dear readers, excelsior!

Last time we discussed what the debt to income ratio was and how it effects one’s overall financial picture. This time we will discuss another ratio that effects your financial picture. The unsecured debt to income ratio is another important piece to understand your financial situation.

Unsecured debt is different from a secured debt as the debt isn’t tied to a piece of collateral such as a car or house. Types of unsecured debt would be credit cards, personal loans, lines of credit, etc. As such these debts are typically assessed higher interest rates than secured debt because of the risks associated with them in the event of a default of payment from a borrower or bankruptcy risk if the borrower ventured into this route.

The unsecured debt ratio (UDTI) equals the total of unsecured debt divided by the total annual income, multiplied by 100, which converts it to a percentage. For example, say Sarah carries $8,000 of credit card debt, $12,000 in personal loans and her annual income is $80,000. Divide the total unsecured debt of $20,000 by $80,000 to get 0.25. Then, multiply 0.25 by 100 to find that Sarah has an unsecured ratio is 25 percent. If Sarah increases her unsecured debt load her and her income remains the same her UDTI will increase. In the opposite scenario if Sarah’s income increases or her unsecured debt is paid down more her UDTI decreases.

Lenders don’t like to make additional unsecured loans to people with high existing unsecured ratios because that’s tacking on additional debt to someone who’s already overextended. Financial institutions often see unsecured ratios of above about 20% as potentially dangerous. When someone gets above 20 percent, the prospective lender might lower the amount it will lend or require the borrower to put up collateral. If the borrower exceeds 30 percent, they will likely encounter trouble just getting an unsecured loan, because lenders are concerned with the ability to repay and there is more risk associated with lending unsecured vs secured. It is ideal to be in a range that is reasonable for a borrowers existing debt and income level and to go beyond that could indicated many factors such as living off of credit cards and unsecured debt to a point where eventually it leads to an eventual endpoint of defaults, garnishments or legal actions to recoup losses from a borrower or even bankruptcy filled by a borrower who is unable to pay. None of which are a desirable outcome for the institution or the borrow to end up.

The unsecured debt to income ratio is an important snapshot of one’s financial picture in the eyes of a lender. It is important to know how it can help or hurt your overall credit and financial situation. I have included a link to assist in calculating your unsecured debt to income ratio as well. Please uses these tools to help with understanding where you are with your own debts to gain a firm grasp on what was covered today. Until the next time dear reader. Excelsior!

You hear about it, you probably pay it, you probably get paid in it. Love it or hate it we are going to talk about interest, what it is and how to make sense of it. Interest is a simple concept but there is often misconceptions about it and confusion. Let us get started in debunking that confusion.

Interest is payment from a borrower or deposit taking institution (such as a bank) to either a lender (someone who you took out a loan from) or a depositor (someone who puts money in the bank) above the principal sum (the original amount of the loan or deposit).at a particular rate. It’s not like a fee which gets paid to a lender and it is not like a dividend that is paid to a shareholder. When interest is paid to a lender or a person depositing money in an interest-bearing account more money comes out on the principal balance. The rate of interest is equal to the interest amount paid or received over a particular period divided by the principal sum borrowed or lent usually expressed by a percentage (such as the annual percentage rate for loans or average percentage yield on interest bearing savings). Wen dealing with interest you also have compound interest (this is the fun one to get paid but not so fun if you are the one paying) which makes the total amount of the debt grow. Interest can be compounded daily, monthly, or on a yearly basis and the impact is affected by the compounding rate.

When dealing with interest you have some rules of thumb to consider. First, the rule of 78s which helps with calculating interest during the life of the loan as you pay on it. (i.e. on a 1 year loan in the 1st month 12/78 of all interest owed over the life of the loan is due and so on and so forth until the 12th month where only 1/78 of all interest is due. The rule of 72 can be used to approximate how long it would take for money to double at a given interest rate, for the compounding interest to reach or exceed the initial deposit, divide 72 by the percentage interest rate. When dealing with interest you always have options to refinance as well as find interest bearing accounts for higher interest to be paid. There are more technical aspects to interest as one looks into the markets and economics outside of the simple aspects of getting pair or paying interest but that is a topic for another time.

Until the next time, stay safe and continue to learn. Excelscior!

/GettyImages-140671550-56a636e83df78cf7728bdbc1.jpg)