/GettyImages-140671550-56a636e83df78cf7728bdbc1.jpg)

You hear about it, you probably pay it, you probably get paid in it. Love it or hate it we are going to talk about interest, what it is and how to make sense of it. Interest is a simple concept but there is often misconceptions about it and confusion. Let us get started in debunking that confusion.

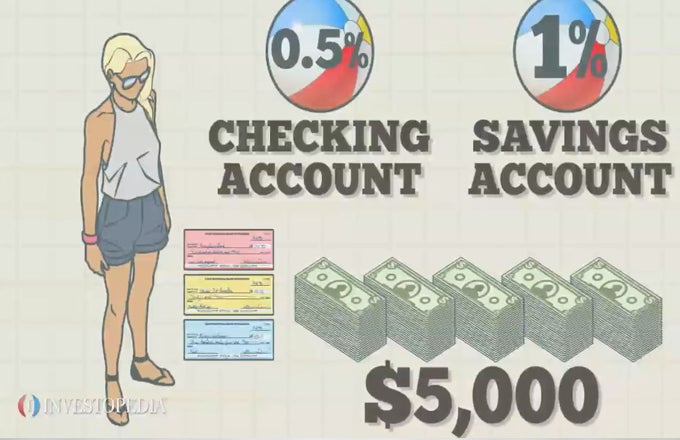

Interest is payment from a borrower or deposit taking institution (such as a bank) to either a lender (someone who you took out a loan from) or a depositor (someone who puts money in the bank) above the principal sum (the original amount of the loan or deposit).at a particular rate. It’s not like a fee which gets paid to a lender and it is not like a dividend that is paid to a shareholder. When interest is paid to a lender or a person depositing money in an interest-bearing account more money comes out on the principal balance. The rate of interest is equal to the interest amount paid or received over a particular period divided by the principal sum borrowed or lent usually expressed by a percentage (such as the annual percentage rate for loans or average percentage yield on interest bearing savings). Wen dealing with interest you also have compound interest (this is the fun one to get paid but not so fun if you are the one paying) which makes the total amount of the debt grow. Interest can be compounded daily, monthly, or on a yearly basis and the impact is affected by the compounding rate.

When dealing with interest you have some rules of thumb to consider. First, the rule of 78s which helps with calculating interest during the life of the loan as you pay on it. (i.e. on a 1 year loan in the 1st month 12/78 of all interest owed over the life of the loan is due and so on and so forth until the 12th month where only 1/78 of all interest is due. The rule of 72 can be used to approximate how long it would take for money to double at a given interest rate, for the compounding interest to reach or exceed the initial deposit, divide 72 by the percentage interest rate. When dealing with interest you always have options to refinance as well as find interest bearing accounts for higher interest to be paid. There are more technical aspects to interest as one looks into the markets and economics outside of the simple aspects of getting pair or paying interest but that is a topic for another time.

Until the next time, stay safe and continue to learn. Excelscior!