In my last entry, I went over what IRAs are and why they matter. This entry will cover contributions to your IRA. You can’t retire without money and to fund an IRA you need to make sure you’re able to stay within certain limits set in place by the IRS. I know what some of you are thinking: “why do I have to limit what I put into my IRA? It’s my retirement money after all!” rest assured I will explain what this entails shortly.

As of this year, the IRS limits up to $6000 to be placed into an IRA each calendar year for regular contributions and $1000 max for catch up distributions. People with eligible compensation (like your earnings from work) of less than their max contribution can only contribute into their IRA equal to their work wages. You can also own a traditional and a Roth IRA, but you cannot go past the $6000 annual limit. Additionally, if you’re 50 or older before the end of the tax year you can make a catch-up contribution into your IRA as well. The deadline for contributions (regular, catch-up, prior year, etc.) is April 15th to the following calendar year.

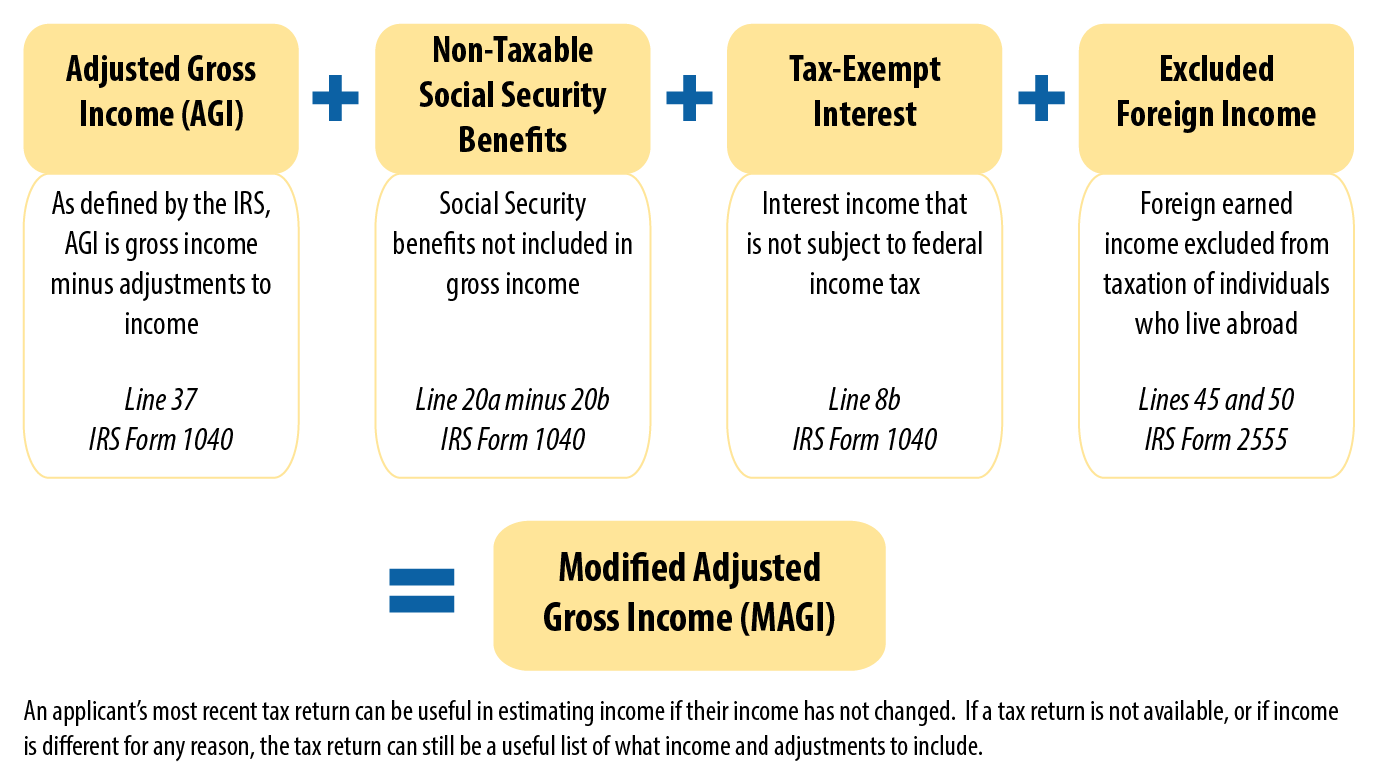

To contribute to a traditional IRA, you must be less than 70 ½ years old and eligible earned funds (usually from work) to place into the IRA. The same rule applies if your spouse wishes to contribute to your IRA but in addition, they must file joint on their tax return with you. Now there are factors regarding your contribution regarding deductions on your taxes. Such factors include having an employer sponsored retirement plan (i.e. 401k), marital status and modified adjusted gross income. Your financial custodian over your IRA cannot determine or track deductible contributions so keep that in mind as you contribute this will need to be done yourself. To further break down modified adjusted gross income you will want to make sure to account for having an employer sponsored retirement plan because there are different ranges for those different income tiers. The same rules apply to Roth IRAs as well. Roth IRA accounts can also receive transfer contributions, rollovers, and conversions (from traditional to Roth and vice versa). Your income has phase out ranges for Roth IRA contribution eligibility, this means however much you make could disqualify you for making a Roth IRA contribution. If your adjusted gross income is within the proper phase out range, however, the eligible contribution amount for a person is reduced. These levels can vary from year to year.

For financial organizations accepting IRA contributions it is required that they keep records of the contributions, the type and the year it was made. This is important for your records and on a typical form for collecting information you’ll see things pertaining to the IRA type, how much you’re putting in, the contribution type and when it was made, as well as any other info including your signature for the records. These contributions can also be reported to the IRS via a form 5498 and have their own tax form for each year you contribute. this information is compared to an individual’s income tax return to determine what’s taxable or tax advantaged as well. Under some state laws it is possible to have a saver’s credit for contributions (see your states contribution rules for this). Typically. these are low to moderate income individuals and the credit is typically nonrefundable and not to exceed $1000. This is based on the annual adjusted gross income figures calculated by the IRS and cost of living adjustments. To be eligible you must be 18 before the end of the tax year (April 15th), not be a dependent or full-time students (sorry kiddos) and have adjusted gross income in the acceptable limits (depending on the year this could vary). This info can be found on the IRS publication 590-A and 8880 for credit for qualified retirement savings contributions.

I knew I threw a lot of material at you today, I wanted to condense this as best as possible. Tune in next time when I discuss the distributions from an IRA and what that means to you. Until then, invest wisely my friends, ciao!

![]()